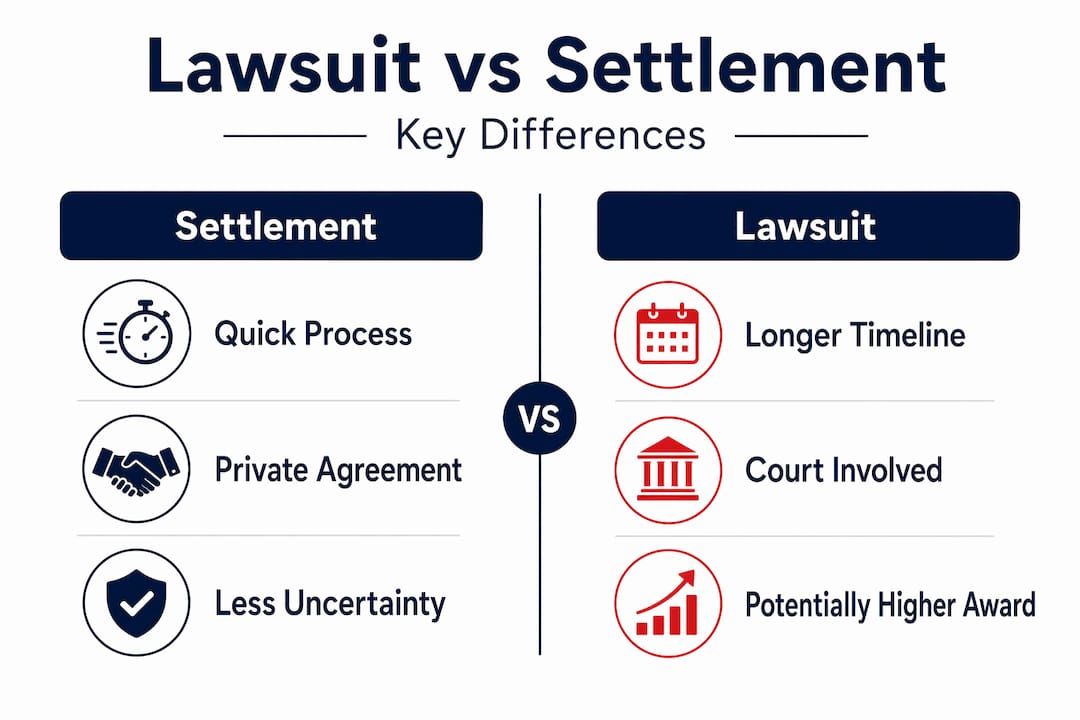

Most people walk away from a car crash with two questions: "How do I pay for this?" and "Should I take the money or sue?" The car accident lawsuit versus settlement explained debate is one of the most misunderstood areas of personal injury law. Many victims assume settling is always faster and suing always means a courtroom drama. Neither is automatically true. The path that gets you fairly compensated depends on the details of your case, your injuries, and how the insurance company behaves. This guide breaks all of it down so you can make a clear, confident decision.

Table of Contents

- Key Takeaways

- How car accident settlements work

- When a lawsuit makes sense

- Deciding between settlement and a lawsuit

- Financial outcomes and legal finality

- Practical tips for navigating your claim

- My honest take on the lawsuit versus settlement decision

- Get free help navigating your car accident claim

- FAQ

Key Takeaways

| Point | Details |

|---|---|

| Settlement is not always faster | Complex injuries can stretch the settlement process to 18 months or longer, rivaling some lawsuits. |

| Lawsuits create negotiation pressure | Filing a lawsuit often pushes insurers to offer more money without ever going to trial. |

| Never settle before maximum medical improvement | Settling too early locks in a number before you know the full cost of your injuries. |

| Settlement releases are permanent | Once you sign, you cannot reopen the claim, even if new symptoms appear later. |

| Legal help changes outcomes | An attorney evaluating your case before you decide can prevent costly mistakes in either direction. |

How car accident settlements work

A settlement is a private agreement between you and the at-fault party's insurance company. You accept a lump sum payment in exchange for releasing all future claims related to the accident. No judge, no jury. Just negotiation, signatures, and a check.

The car accident settlement process generally moves through these stages:

- Complete medical treatment (or reach maximum medical improvement): You should not negotiate until your doctors know the full extent of your injuries. Settling early caps the insurer's exposure before your total costs are known.

- Send a demand letter: Your attorney (or you, if unrepresented) sends a detailed letter outlining your injuries, medical costs, lost wages, and pain and suffering.

- Negotiate with the adjuster: The insurer responds, usually below your demand. You counter. This exchange can repeat several times.

- Reach an agreement: Once both sides agree on a number, you sign a release document.

- Receive payment: Insurers typically pay within 10 to 30 days after the signed release, though lien resolution (repaying health insurance or medical providers) adds additional weeks before the money reaches you.

Timelines vary widely. Minor injury cases often resolve in 2 to 6 months; serious injuries can take 6 months to well over a year. Check the claim timeline guide for a visual breakdown of what to expect.

One thing most victims do not expect: the adjuster is not on your side. Insurance adjusters intentionally offer fractions of true claim value to test whether you know what your case is actually worth. That first offer is almost always a test, not a fair number.

Pro Tip: Do not respond to a first offer with a counter the same day. Wait, review your full medical bills and lost wages, and respond in writing with documented justification for your number.

When a lawsuit makes sense

Filing a lawsuit means formally taking your claim to court by submitting a legal complaint against the at-fault driver. It sounds dramatic, but over 90% of personal injury cases settle without ever reaching trial. The lawsuit itself is often the tool that forces a real negotiation, not a sign that you are heading to a courtroom.

Reasons people choose to file a lawsuit include:

- The settlement offer is far below actual damages. If medical bills alone exceed what the insurer is offering, negotiation alone may not close the gap.

- Liability is disputed. The insurer is blaming you or denying the claim outright.

- The injury is severe or permanent. High-stakes cases involving surgery, long-term disability, or significant lost income often require legal pressure to resolve fairly.

- The insurer is stalling. Some companies delay on purpose, hoping you will get desperate and accept less.

- The statute of limitations is approaching. Florida reduced its deadline from 4 to 2 years, and many states have similar limits. Filing preserves your legal rights even if you hope to settle.

Once a lawsuit is filed, the case enters a phase called discovery. Both sides exchange documents, interview witnesses, and build their arguments. This process alone often prompts insurers to reassess and raise their offer. Filing suit forces insurers to allocate reserves and negotiate seriously, which is why many attorneys use it as a deliberate strategy rather than a last resort.

The tradeoff is time. Litigation adds months to your case, sometimes years if it reaches trial. Lawsuit timelines in complex or disputed cases can extend 1 to 4 years beyond the accident date.

Pro Tip: Filing a lawsuit does not mean you want a trial. Most accident attorneys file with the intention of settling at a higher number after the insurer sees the legal cost they now face.

Deciding between settlement and a lawsuit

This is where most people get stuck. The right path depends on your specific situation, not a general rule. Here is a side-by-side comparison of the key factors:

| Factor | Lean toward settlement | Lean toward lawsuit |

|---|---|---|

| Injury severity | Minor to moderate, fully healed | Severe, permanent, or still progressing |

| Liability clarity | Fault is clear and documented | Liability is disputed |

| Insurer behavior | Reasonable offers, good faith negotiation | Lowballing, delaying, or denying |

| Financial urgency | You need resolution soon | You can afford to wait for full value |

| Medical status | You have reached maximum medical improvement | Still treating, costs unknown |

| Offer versus damages | Offer covers medical costs, lost wages, and pain | Offer falls far short of actual losses |

The most critical variable is maximum medical improvement (MMI). This is the point where your doctor confirms your condition has stabilized. Settling before MMI almost always results in leaving money on the table because future care costs are not yet known.

You also need to know how long you have to file in your state. Dragging out settlement talks past your deadline eliminates your lawsuit option entirely. That is one of the most avoidable and costly mistakes in car accident claims.

If the settlement offer fairly covers your medical costs, lost wages, and pain and suffering, accepting it is often the efficient move. If the offer falls short of your documented damages, litigation becomes the path to enforcing fair value.

Financial outcomes and legal finality

Understanding the money side matters just as much as understanding the process. Here is what each path looks like financially:

Settlement financial breakdown:

- Gross settlement amount (what you and the insurer agree to)

- Minus attorney fees (typically 33% to 40% on contingency)

- Minus medical liens (repayment to health insurers or providers)

- Minus case costs (filing fees, expert reports, medical records)

- Equals your net payment

Lawsuit and trial financial considerations:

- Potential for a higher jury verdict, though not guaranteed

- Trials introduce uncertainty and remove control from both parties

- Attorney fees may increase if the case goes to trial

- Longer timeline means delayed compensation

One point that cannot be overstated: settlement releases are legally final and irreversible. Once you sign, you cannot go back. If you develop complications from your injuries a year later, that claim is closed. Review every word of the release before signing, and have an attorney review it with you if at all possible.

Use WreckMatch's case value guide to benchmark what a fair offer should look like before you make any decisions.

Practical tips for navigating your claim

Whether you settle or sue, the actions you take right now affect the outcome.

- Document everything. Every doctor visit, prescription, missed workday, and out-of-pocket expense strengthens your claim in either direction.

- Do not talk to the other driver's insurer without guidance. Adjusters are trained to get statements that reduce your payout. Read up on dealing with insurance adjusters before you take that call.

- Do not accept the first offer. The first offer is rarely the final offer. Countering with documented evidence almost always moves the number up.

- Know your state's statute of limitations. Do not let the clock run out while waiting for a "better" offer that may never come.

- Get legal help early. An experienced personal injury attorney evaluates your case before you commit to a path, at no upfront cost in most cases.

If you are unsure where you stand right now, start with the accident steps guide to make sure the foundation of your claim is solid.

My honest take on the lawsuit versus settlement decision

I have talked to hundreds of people after car accidents. The most common regret I hear is not "I wish I had gone to trial." It is "I settled too fast."

Victims who accept early offers before they finish treatment almost always leave money behind. An insurer offering $8,000 two weeks after the accident on a case with an unresolved back injury is betting you do not know what that injury might cost long-term. And they are usually right, unless you get good advice.

Here is what I have found actually matters: the lawsuit versus settlement question is almost never about going to trial. It is about leverage. Filing a lawsuit changes the insurer's math. Suddenly, they have legal fees, discovery costs, and reserve requirements to deal with. That pressure moves settlement numbers in ways that phone negotiation alone rarely does.

My take is this: if you have a clear liability case, documented injuries, and an insurer making low offers, filing a lawsuit is often a smarter tool than a strategy of last resort. Most cases still settle. They just settle for more. The attorneys at Lydon Law put it plainly in their breakdown of accident cases: the decision to sue is often the decision to negotiate from a position of strength.

Evaluate your case on its own facts. Do not assume settlement is the easy path or that a lawsuit means years of stress. Talk to an attorney before you decide anything.

— Scott

Get free help navigating your car accident claim

If this article raised more questions than it answered, that is normal. The car accident settlement process has enough variables that even well-informed victims benefit from a professional review before committing to a path.

WreckMatch connects you with experienced personal injury attorneys at no upfront cost. No fees unless you win. You can get matched in under 60 seconds using the free attorney matching service. If you want to keep learning first, the accident survival guide covers everything from the crash scene to your final check, and the free weekly webinars let you ask real questions live. You deserve to know what your case is worth before you sign anything.

FAQ

What is the difference between a settlement and a lawsuit?

A settlement is a private agreement with the insurer that resolves your claim without court involvement. A lawsuit is a formal legal action filed in court, though most lawsuits still end in settlement before trial.

How long does a car accident settlement take?

Minor injury cases often resolve in 2 to 6 months, while serious injury cases can take over a year. If litigation is needed, the timeline can extend to 1 to 4 years.

Should I accept the first settlement offer from the insurance company?

No. Insurers intentionally offer low amounts initially to test your knowledge and financial pressure. Counter with documented proof of your actual damages before agreeing to anything.

Can I reopen a claim after settling?

No. Settlement releases are permanent and legally binding. Once you sign, the claim is closed regardless of any symptoms or costs that arise later.

When should I hire a lawyer for a car accident claim?

Hire a lawyer as early as possible, especially for serious injuries, disputed liability, or low settlement offers. Most personal injury attorneys work on contingency, meaning there is no cost to you unless they win your case.