A catastrophic injury structured settlement is a legally binding financial arrangement that delivers tax-free, periodic payments to injury victims in place of a single lump sum. Under IRC Sections 104(a)(2) and 130, every dollar of principal and interest paid through a qualifying physical injury settlement is 100% exempt from federal income tax. For anyone facing lifelong medical costs after a spinal cord injury, traumatic brain injury, or severe burn, this structure is not a convenience. It is a financial lifeline. This catastrophic injury structured settlement guide covers how these arrangements work, what protections they carry, how to plan yours correctly, and what mistakes can cost you everything.

How does a catastrophic injury structured settlement work?

A structured settlement converts your injury compensation into a guaranteed payment stream funded by a life insurance company. The process follows a clear sequence:

- Negotiation. Your attorney and the defendant's insurer agree on a total settlement amount and a payment schedule. This schedule defines how much you receive, how often, and for how long.

- Qualified assignment. The defendant transfers its payment obligation to a third-party assignment company. This step is required under IRC Section 130 to preserve the tax exemption.

- Annuity purchase. The assignment company uses the settlement funds to buy a structured settlement annuity from a highly rated life insurance company. That insurer becomes the obligor, meaning it is legally responsible for every future payment.

- Payment delivery. The life insurance company sends payments directly to you on the agreed schedule, whether monthly, quarterly, or annually, for the duration of the contract.

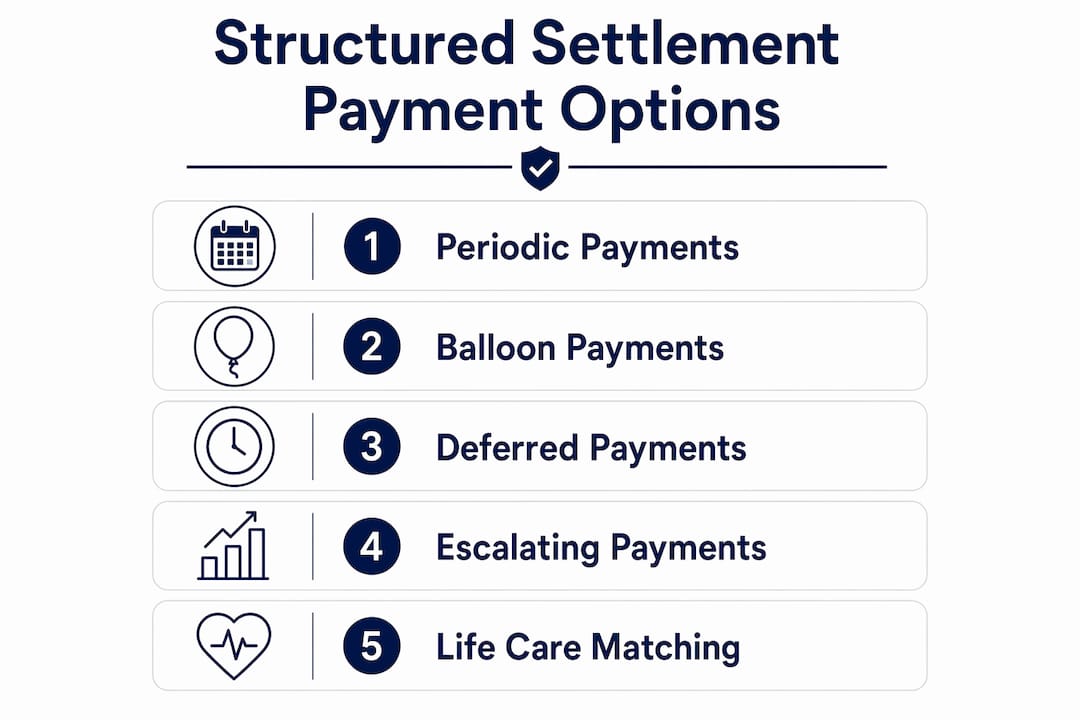

You can customize the payment structure in several ways. Common options include period certain payments (guaranteed for a fixed number of years regardless of whether you survive), life-contingent payments (continuing for your lifetime), deferred lump sums called balloon payments (large one-time amounts scheduled for future dates to cover anticipated expenses), and escalating payment streams that increase annually to keep pace with inflation.

Pro Tip: Ask your attorney to include at least one balloon payment timed to coincide with a major anticipated expense, such as home modification costs or a wheelchair replacement cycle. This single step prevents a cash crisis years down the road.

What are the tax benefits and legal protections of structured settlements?

The tax treatment of structured settlements is one of their most powerful features. Under federal tax law, the entire payment stream, including the interest component that accumulates over decades, is received tax-free. A lump sum invested in stocks or bonds generates taxable gains every year. A structured settlement generates none. For a settlement worth $3 million paid out over 30 years, the tax savings can exceed the original principal.

Key protections include:

- Full federal tax exemption. IRC Section 104(a)(2) covers both principal and interest for physical injury claims. This applies to car accident injuries, workplace injuries, and medical malpractice resulting in physical harm.

- Court approval for vulnerable claimants. Judges review payment schedules in cases involving minors or incapacitated adults, confirming that the payment plan serves the claimant's long-term interests and that funds will not be depleted prematurely.

- Creditor protection. Payments are shielded from most creditors, protecting your income stream even if you face financial hardship later.

- Exploitation prevention. The periodic payment structure prevents third parties from pressuring you into handing over a large lump sum.

One critical limitation: the tax exemption applies only to physical injury claims. Settlements for emotional distress alone, without an accompanying physical injury, do not qualify. If your claim combines physical and emotional harm, proper allocation in the settlement agreement is required to protect the exemption on the physical portion. For state-specific tax questions, resources like Oaks Law Firm's tax overview explain how California and other states treat these payments.

"Structured settlements serve as a vital safeguard against financial exploitation and maintain claimants' long-term welfare." — Martin Helms Law

How to plan and customize your settlement for long-term needs

Planning a structured settlement for a catastrophic injury is not a one-hour conversation. It requires detailed financial modeling, medical forecasting, and coordination with multiple professionals. Getting this right at the start matters because settlement terms are irrevocable once the annuity contract is issued.

Start with a life care plan

A life care plan is a document prepared by a certified life care planner that projects every medical cost you will face over your lifetime. It covers surgeries, therapies, medications, home health aides, adaptive equipment, and housing modifications. Working with a dedicated life care planner is the single most effective way to prevent underfunding. Underestimating future medical inflation by even 2% annually can leave a 40-year-old spinal cord injury survivor hundreds of thousands of dollars short by age 65.

Match payment streams to anticipated expenses

| Payment type | Best use case |

|---|---|

| Monthly base payments | Ongoing living expenses and routine medical costs |

| Escalating annual payments | Inflation protection for long-term care costs |

| Deferred balloon payments | Scheduled large expenses like home renovations or equipment replacement |

| Period certain guarantee | Income protection for dependents if you pass away early |

| Life-contingent payments | Maximum income if you have a normal or extended life expectancy |

Tailored payment structures involving deferred and escalating streams consistently outperform flat monthly payments for complex long-term care needs. Financial modeling that maps your projected expenses against each payment option is not optional. It is the foundation of a sound settlement.

Integrate Medicare Set-Asides and public benefits

If you receive Medicare or Medicaid, or expect to qualify in the future, your settlement must account for a Medicare Set-Aside (MSA). An MSA is a portion of your settlement funds set aside specifically to pay for injury-related medical expenses that Medicare would otherwise cover. Ignoring MSA requirements risks Medicare payment denials for future injury-related care and potential double damages. Your attorney should coordinate with a Medicare compliance specialist before finalizing any settlement.

Pro Tip: Keep a portion of your settlement outside the structured annuity as liquid cash, typically three to six months of living expenses. This covers emergencies that fall between scheduled payments without forcing you to sell future payment rights at a steep discount.

What common mistakes do catastrophic injury victims make with structured settlements?

The most expensive errors in structured settlement planning happen before the ink dries. Once the annuity contract is issued, terms cannot be modified. The following mistakes are the most common and the most preventable:

- Over-structuring all funds. Placing 100% of your settlement into the annuity leaves no cash for immediate needs like home modifications, vehicle adaptations, or legal fees. Always retain a liquid reserve.

- Skipping balloon payments. Flat monthly payments feel predictable but fail to account for large future costs. A wheelchair costs $25,000 to $50,000 and needs replacement every five years. Plan for it explicitly.

- Ignoring Medicare coordination. Failing to integrate an MSA can result in Medicare refusing to pay for injury-related care until the entire settlement is spent down. This is a catastrophic outcome that proper planning prevents.

- Choosing the wrong payment start date. Many victims need immediate income. Others have short-term disability coverage and benefit more from deferred payments that grow larger over time. Match the start date to your actual income gap.

- Settling without specialized counsel. A general practice attorney may not understand structured settlement mechanics, life care planning, or MSA compliance. Catastrophic injury cases require attorneys who work in this area specifically. If you suffered injuries in a serious crash, reviewing post-injury legal steps before accepting any offer is critical.

Settlements exceeding $2 million were historically spent within a few years when paid as lump sums, leading to financial ruin. The structured settlement model exists precisely because that pattern repeated itself often enough to demand a systemic solution.

Key takeaways

A catastrophic injury structured settlement delivers guaranteed, tax-free income for life, but only when planned with a life care planner, Medicare compliance specialist, and a catastrophic injury attorney working together from the start.

| Point | Details |

|---|---|

| Tax-free payment stream | IRC Section 104(a)(2) exempts all principal and interest from federal income tax for physical injury claims. |

| Irrevocable terms | Settlement terms cannot be changed after the annuity is issued, so build flexibility in before signing. |

| Life care plan is required | A certified life care planner must project lifetime medical costs to prevent underfunding. |

| Medicare Set-Aside compliance | Ignoring MSA requirements risks Medicare payment denials and severe financial penalties. |

| Retain liquid reserves | Keep three to six months of expenses outside the annuity to cover emergencies between payments. |

What I've learned from watching catastrophic injury settlements go wrong

I have seen the same pattern repeat itself more times than I can count. A family accepts a settlement that looks generous on paper. The monthly payments feel comfortable. Then, five years later, the victim needs a power wheelchair, a home elevator, or a round-the-clock aide. The payment schedule has no balloon. There is no cash reserve. The family is forced to sell future payment rights to a factoring company at a 40% to 60% discount.

Predictability beats market potential every time in catastrophic injury cases. I do not care what the stock market returned last year. A 35-year-old with a spinal cord injury cannot afford a down year. The structured settlement exists to remove that risk entirely, and that is its greatest strength.

What I push back on is the idea that any structured settlement is automatically a good one. The structure is only as good as the planning behind it. A flat monthly payment with no escalation and no balloons is not a plan. It is a slow-motion funding crisis. The victims who fare best are the ones whose attorneys brought in a life care planner and a Medicare compliance specialist before the first settlement offer was even countered.

If you are reading this after a serious crash, do not let urgency push you into a settlement that has not been fully modeled. The defendant's insurer is not your financial planner. Get your own team. The difference between a well-structured settlement and a poorly structured one can be measured in millions of dollars over a lifetime.

— Scott

How WreckMatch helps you find the right legal team

Navigating catastrophic injury compensation alone is overwhelming. WreckMatch connects accident victims with experienced personal injury attorneys who handle structured settlements, life care planning coordination, and Medicare compliance, at no upfront cost to you.

WreckMatch's Accident Survival Guide breaks down every stage of the legal and financial process in plain language, from your first call to final settlement. If you were injured in a serious crash in cities like Philadelphia or Chicago, WreckMatch's free attorney matching connects you with a licensed catastrophic injury lawyer in 60 seconds. No upfront cost. No confusion. Just fast, qualified help when you need it most.

FAQ

What is a structured settlement for a catastrophic injury?

A structured settlement for a catastrophic injury is a legally binding agreement that pays compensation in periodic installments rather than a single lump sum. Payments are 100% tax-free under IRC Section 104(a)(2) when the claim involves physical injury.

Can structured settlement terms be changed after signing?

No. Structured settlement terms are irrevocable once the annuity contract is issued. Any flexibility, such as balloon payments or escalating streams, must be built into the agreement before it is finalized.

What is a Medicare Set-Aside in a structured settlement?

A Medicare Set-Aside (MSA) is a portion of your settlement funds reserved to pay for injury-related medical expenses that Medicare would otherwise cover. Failing to include a proper MSA can result in Medicare denying future injury-related claims.

How does a structured settlement differ from a lump sum?

A lump sum delivers all compensation at once, creating tax liability on investment gains and the risk of rapid depletion. A structured settlement delivers guaranteed, tax-free payments over time, protecting long-term financial stability.

Do I need a specialized attorney for a catastrophic injury settlement?

Yes. Catastrophic injury cases require attorneys experienced in structured settlement mechanics, life care planning, and Medicare compliance. A general practice attorney may miss critical planning elements that cost you significantly over your lifetime.

Recommended

- Catastrophic Injury Car Crash in Chicago, Illinois (2026) | WreckMatch Blog | WreckMatch

- Catastrophic Injury Car Crash in Atlanta, Georgia (2026) | WreckMatch Blog | WreckMatch

- Catastrophic Injury Car Crash in San Antonio, Texas (2026) | WreckMatch Blog | WreckMatch

- Catastrophic Injury After a Car Crash — Next Steps (2026) | WreckMatch Blog | WreckMatch