Catastrophic injury insurance coverage limits are defined as the maximum dollar amount an insurer will pay for losses resulting from a severe, life-altering injury. These limits directly control how much money you receive for medical care, rehabilitation, and attendant support after a serious accident. Coverage can range from $65,000 for standard injuries to $1,000,000 or more for catastrophic designations, depending on your policy and jurisdiction. In Ontario and Michigan, the rules differ significantly, and knowing those differences is the first step toward protecting your claim. This article has catastrophic injury insurance coverage limits explained in plain terms, so you can act with clarity instead of confusion.

How do catastrophic injury coverage limits work in ontario?

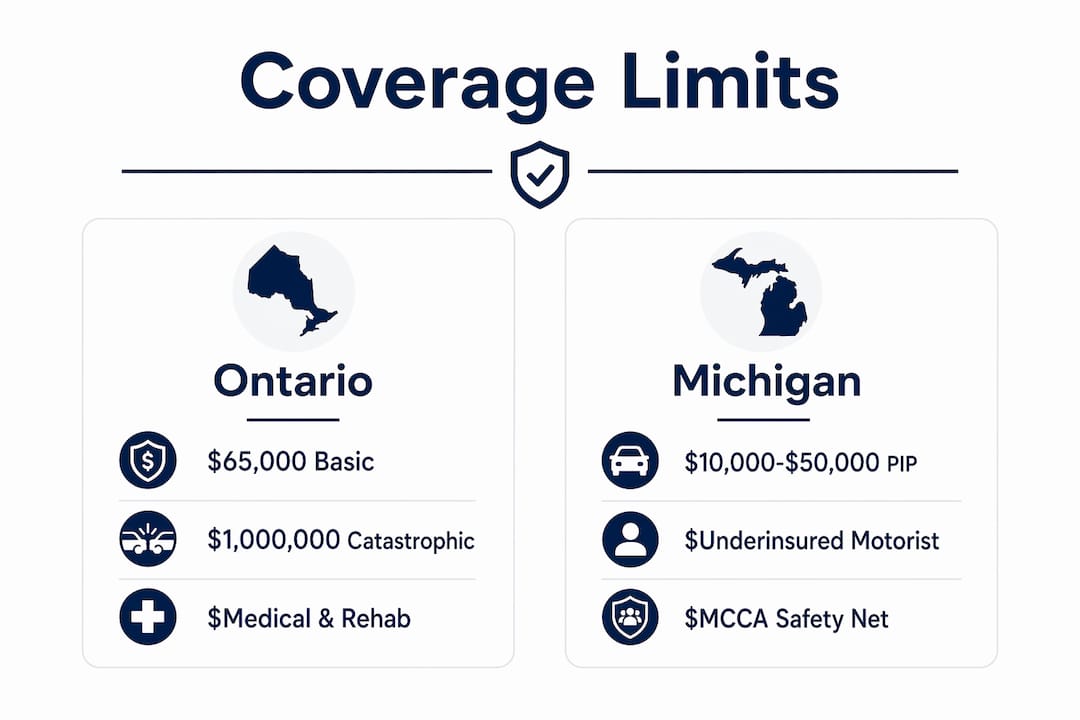

Ontario's auto insurance system uses a legal designation called catastrophic impairment under the Statutory Accident Benefits Schedule (SABS). This designation is the trigger that unlocks dramatically higher benefit limits for injured people. Without it, your medical, rehabilitation, and attendant care benefits are capped at $65,000 for non-catastrophic injuries. With it, that limit rises to $1,000,000, available for your lifetime or until the funds are exhausted.

That difference is not just a number. It determines whether you can afford long-term home care, specialized equipment, or ongoing therapy after a spinal cord injury, traumatic brain injury, or severe amputation. The catastrophic impairment label in Ontario legally unlocks a completely different tier of support.

Here is what the designation affects:

- Medical and rehabilitation benefits: Increase from $65,000 to $1,000,000

- Attendant care benefits: Monthly limits increase significantly, covering in-home support for daily living

- Benefit duration: Catastrophic benefits remain available for life, not just a fixed term

- Tort claims: A catastrophic designation can also strengthen your right to sue for additional damages beyond accident benefits

The challenge is that insurers can dispute the designation, and those disputes go through Ontario's Licence Appeal Tribunal. That process takes time, and every delay means you are operating under the lower $65,000 cap while your case is pending.

Pro Tip: Start gathering detailed medical records, functional assessments, and specialist reports from day one. Thorough documentation is the single most important factor in securing a catastrophic designation quickly and successfully.

Incomplete or poor documentation can delay or completely block access to the $1,000,000 benefit level. Do not leave this to chance.

What are michigan's PIP tiers for severe injury claims?

Michigan operates under a no-fault auto insurance system built around Personal Injury Protection (PIP) coverage. Since 2020, Michigan drivers choose their own PIP tier, and that choice directly caps how much the insurer pays for crash-related medical care. The three main options are:

- $250,000 PIP limit: The insurer pays up to $250,000 in medical expenses per accident. After that, you are on your own.

- $500,000 PIP limit: Doubles the protection, but still carries a hard ceiling that catastrophic injuries can exhaust within months.

- Unlimited PIP coverage: Removes the dollar cap entirely. The insurer pays all reasonable and necessary medical costs for life.

Michigan's tiered PIP system means your coverage ceiling was set before your accident happened, based on a decision you may not have fully understood at the time. That is a critical point. A spinal cord injury requiring lifetime care can cost well over $1,000,000 in the first decade alone. A $250,000 limit disappears fast.

Michigan also has a safety net called the Michigan Catastrophic Claims Association (MCCA). This organization reimburses insurers for unlimited PIP claims that exceed a set threshold. It only applies to drivers who selected unlimited PIP coverage. If you chose a $250,000 or $500,000 tier, the MCCA provides no protection once your limit runs out.

Pro Tip: Check your insurance declarations page right now to confirm which PIP tier you selected. Many people chose a lower tier to save on premiums and do not realize the risk until after a serious accident.

Michigan injury attorneys consistently stress that verifying your PIP tier immediately after an accident is one of the most important steps you can take. You need to know your ceiling before you can plan around it. For more on Michigan-specific coverage challenges, Wreckmatch has a detailed resource on Michigan PIP claim issues.

What happens when your coverage limits run out?

When your primary insurance coverage is exhausted, other layers of protection can step in. Understanding this stacking system is central to understanding injury coverage limits in catastrophic cases.

PIP benefits in many no-fault states typically range from $10,000 to $50,000, which is nowhere near enough for catastrophic injuries. Even Michigan's $250,000 tier can be gone within a year of serious care. Here is how the coverage layers typically work:

| Coverage Layer | What It Covers | Typical Limit |

|---|---|---|

| PIP / No-Fault Benefits | Medical, lost wages, attendant care | $10,000–Unlimited (varies by state) |

| Liability Coverage (at-fault driver) | Damages caused to others | $25,000–$1,000,000+ |

| Underinsured Motorist (UIM) | Gap when at-fault driver's limits are too low | Matches your own policy limit |

| Umbrella / Excess Policy | Extends above primary policy limits | $1,000,000–$5,000,000+ |

| Health Insurance | Medical bills not covered by auto insurance | Varies by plan |

| Workers' Compensation | If injury occurred during employment | Varies by state |

Primary liability coverage pays first, then underinsured motorist (UIM) coverage responds when the at-fault driver's limits are too low to cover your losses. Umbrella policies extend above your primary limits, but they come with conditions.

One major misconception is that umbrella policies automatically cover all catastrophic claims. Umbrella coverage requires that you maintain the underlying policies at required levels, and not every claim qualifies. Read your umbrella policy carefully before assuming it applies.

Practical steps to take when limits are at risk of being exhausted:

- Notify all relevant insurers in writing as soon as possible

- Request a full copy of every applicable policy, including umbrella and excess policies

- Confirm whether your health insurer has a subrogation right against your settlement

- Consult a catastrophic injury specialist attorney before accepting any settlement offer

Pro Tip: Do not wait until your primary coverage runs out to investigate secondary layers. Identify every available policy within the first 30 days after your accident.

How does medicare affect your catastrophic injury settlement?

Medicare is not a passive bystander in your injury claim. If Medicare paid for any medical treatment related to your accident, it has a legal right to be repaid from your settlement. This is called a Medicare lien, and it is backed by federal law.

The Medicare Secondary Payer statute, codified at 42 U.S.C. § 1395y(b), establishes Medicare as a secondary payer when another source, such as auto insurance or a liability settlement, is available. Medicare pays your bills conditionally, meaning it expects reimbursement once you recover money from another source. Ignoring this obligation can result in double damages and serious legal consequences.

Key points every catastrophic injury claimant needs to know:

- Medicare sends a demand letter once it learns of your settlement. You have 120 days to request a redetermination if you believe the amount is wrong.

- Timely action on Medicare liens is required. Delays increase complications and can reduce your net recovery.

- Conditional payments can be negotiated in some cases, especially when the settlement is limited by policy caps.

- Your attorney must account for Medicare in any settlement strategy. Failing to do so can expose both you and your lawyer to liability.

- Planning for Medicare repayment early in the settlement process prevents costly surprises and protects your net recovery.

The interaction between Medicare and your coverage limits is especially complex in catastrophic cases where multiple insurers are involved. A structured settlement, for example, may need to include a Medicare Set-Aside (MSA) account to cover future injury-related medical costs. Wreckmatch's guide on structured settlement planning covers this in detail.

Key takeaways

Catastrophic injury insurance coverage limits define your financial ceiling after a severe accident, and knowing those limits before they run out is the most important step you can take.

| Point | Details |

|---|---|

| Ontario's catastrophic designation | Raises your benefit limit from $65,000 to $1,000,000 for life, but requires strong medical documentation. |

| Michigan PIP tier selection | Your pre-accident tier choice caps your medical coverage; unlimited PIP is the only option with no ceiling. |

| Coverage stacking matters | When primary limits run out, UIM, umbrella, and health insurance can fill gaps if properly maintained. |

| Umbrella policies have conditions | They do not automatically apply; you must meet underlying policy requirements and claim qualifications. |

| Medicare liens are mandatory | Federal law requires repayment of Medicare conditional payments from any liability settlement you receive. |

What i've learned working with catastrophic injury claims

I have seen the same mistake repeated more times than I can count. Someone suffers a life-changing injury, and the first question they ask is about fault. The question they should be asking is: what are my coverage limits, and how fast will they run out?

Most people have no idea what tier of PIP coverage they selected or whether their umbrella policy actually applies to auto accidents. By the time they find out, they have already made decisions that cannot be undone. Accepted a settlement. Missed a Medicare deadline. Failed to document their injury thoroughly enough to qualify for a catastrophic designation in Ontario.

The coverage limit is not just a number in your policy. It is the boundary of your financial recovery. Everything you do in the first 60 days after a catastrophic injury either expands or shrinks what you can ultimately recover. Early verification, thorough documentation, and legal guidance are not optional steps. They are the difference between a claim that covers your lifetime care and one that runs dry in year two.

I also want to be direct about something most articles skip: the insurance company already knows your limits. Their adjusters are trained to settle claims before you understand the full scope of what you are entitled to. You need someone in your corner who knows the system as well as they do. That is not pessimism. It is just how the process works, and knowing it puts you in a stronger position.

— Scott

Get free legal help for your catastrophic injury claim

Dealing with coverage limits, benefit designations, and Medicare liens is genuinely complex. You should not have to figure it out alone while recovering from a serious injury.

Wreckmatch connects accident victims with experienced personal injury attorneys at no upfront cost. There is no fee unless you win. You can get matched with a licensed attorney in your state in 60 seconds or less. Whether you are dealing with a disputed Ontario catastrophic designation, an exhausted Michigan PIP limit, or a Medicare lien you did not expect, Wreckmatch can help you find the right legal support fast. Visit Wreckmatch to get free attorney matching now, or explore the Accident Survival Guide for more resources built specifically for catastrophic injury survivors.

FAQ

What is a catastrophic injury insurance coverage limit?

A catastrophic injury insurance coverage limit is the maximum dollar amount your insurer will pay for medical, rehabilitation, and related expenses after a severe injury. The specific amount depends on your policy type, state or province, and whether you qualify for an enhanced catastrophic designation.

How much does ontario pay for catastrophic injuries?

Ontario's catastrophic impairment designation raises accident benefits to $1,000,000 for medical, rehabilitation, and attendant care, compared to $65,000 for non-catastrophic injuries. These benefits remain available for life or until the funds are exhausted.

What happens when michigan PIP limits run out?

When your Michigan PIP limit is exhausted, you must rely on other coverage layers such as underinsured motorist coverage, health insurance, or umbrella policies. Drivers who selected unlimited PIP coverage have no dollar cap and are protected by the Michigan Catastrophic Claims Association for lifetime medical costs.

Does medicare have to be repaid from a catastrophic injury settlement?

Yes. Under the Medicare Secondary Payer statute, Medicare must be reimbursed for any conditional payments it made for your injury-related care once you receive a settlement or award. Failing to repay can result in significant legal and financial penalties.

Do umbrella policies automatically cover catastrophic injury claims?

No. Umbrella coverage requires that your underlying policies are maintained at required limits and that the specific claim qualifies under the umbrella policy terms. Not all catastrophic injury claims automatically trigger umbrella coverage.